All Categories

Featured

Table of Contents

Adolescent insurance supplies a minimum of security and might supply insurance coverage, which could not be offered at a later day. Amounts supplied under such protection are typically limited based upon the age of the child. The existing limitations for minors under the age of 14.5 would certainly be the greater of $50,000 or 50% of the quantity of life insurance policy in force upon the life of the candidate.

Adolescent insurance coverage may be sold with a payor benefit rider, which offers for waiving future costs on the child's policy in the event of the death of the individual that pays the costs. Senior life insurance policy, sometimes referred to as graded survivor benefit strategies, gives eligible older applicants with very little whole life protection without a medical examination.

The permissible problem ages for this sort of coverage range from ages 50 75. The optimum problem quantity of protection is $25,000. These plans are typically extra pricey than a completely underwritten plan if the person qualifies as a common danger. This kind of coverage is for a tiny face quantity, typically purchased to pay the funeral expenditures of the insured.

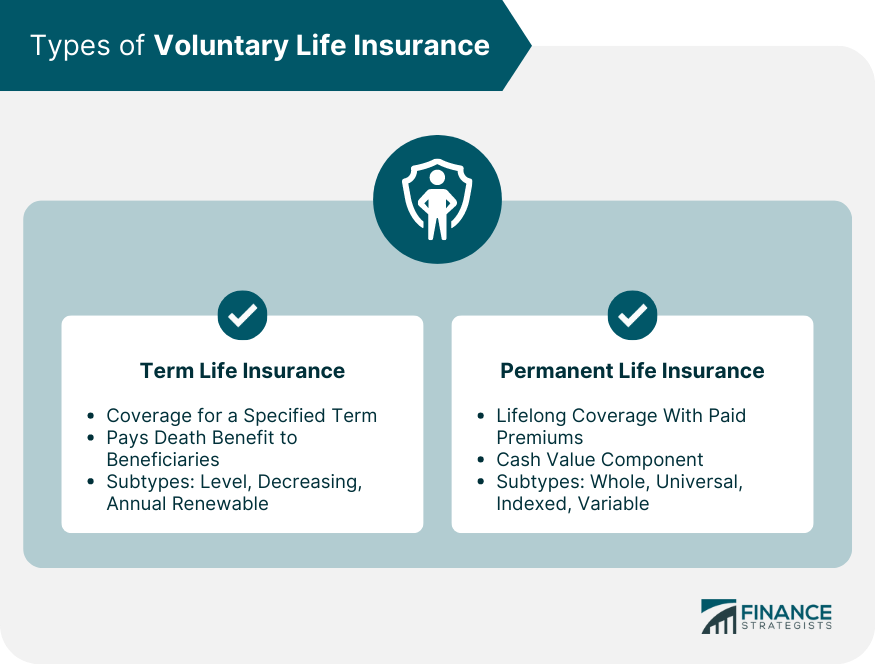

Our term life choices include 10, 15, 20, 25, 30, 35, and 40-year policies. The most preferred type is level term, indicating your repayment (costs) and payment (survivor benefit) stays degree, or the very same, till the end of the term period. This is one of the most uncomplicated of life insurance coverage choices and needs really little upkeep for policy owners.

Level Term Life Insurance For Families

For instance, you can provide 50% to your spouse and divided the rest amongst your adult children, a moms and dad, a good friend, and even a charity. * In some instances the survivor benefit might not be tax-free, discover when life insurance policy is taxable

1Term life insurance policy provides temporary defense for an important duration of time and is normally cheaper than permanent life insurance coverage. 2Term conversion guidelines and constraints, such as timing, may use; for instance, there might be a ten-year conversion opportunity for some items and a five-year conversion advantage for others.

3Rider Insured's Paid-Up Insurance policy Acquisition Alternative in New York. 4Not available in every state. There is a price to exercise this rider. Products and bikers are readily available in approved jurisdictions and names and functions may differ. 5Dividends are not assured. Not all getting involved plan owners are qualified for rewards. For select motorcyclists, the problem uses to the insured.

Term Life Insurance With Fixed Premiums

We may be made up if you click this ad. Advertisement Level term life insurance policy is a policy that offers the very same death advantage at any kind of point in the term. Whether you die on the very same day you get a plan or the last, your beneficiaries will obtain the exact same payout.

Plans can likewise last up until specified ages, which in a lot of instances are 65. Past this surface-level details, having a higher understanding of what these plans involve will certainly aid ensure you buy a policy that fulfills your demands.

Be mindful that the term you select will influence the premiums you pay for the plan. A 10-year level term life insurance policy will set you back much less than a 30-year policy due to the fact that there's less opportunity of an occurrence while the strategy is energetic. Lower danger for the insurance firm equates to decrease premiums for the insurance holder.

Who offers Level Term Life Insurance Coverage?

Your family members's age must likewise influence your policy term option. If you have children, a longer term makes good sense since it secures them for a longer time. If your children are near their adult years and will be financially independent in the close to future, a shorter term might be a much better fit for you than a prolonged one.

When comparing entire life insurance policy vs. term life insurance coverage, it's worth noting that the last generally prices much less than the former. The result is more protection with reduced costs, offering the best of both globes if you require a significant amount of protection however can not afford a more expensive plan.

Why do I need Compare Level Term Life Insurance?

A degree fatality advantage for a term policy usually pays out as a lump amount. Some degree term life insurance policy business enable fixed-period settlements.

Passion settlements received from life insurance policy plans are thought about earnings and are subject to tax. When your degree term life policy expires, a couple of different things can occur.

The disadvantage is that your renewable degree term life insurance will certainly come with higher premiums after its preliminary expiry. We may be made up if you click this ad.

Where can I find Level Term Life Insurance?

Life insurance coverage companies have a formula for calculating threat using death and interest. Insurance firms have countless clients securing term life plans at the same time and make use of the premiums from its active plans to pay surviving beneficiaries of various other policies. These companies make use of mortality tables to approximate the number of people within a particular group will certainly file fatality claims annually, and that details is utilized to figure out typical life span for potential insurance holders.

Furthermore, insurer can invest the cash they obtain from costs and increase their revenue. Since a degree term plan does not have cash value, as an insurance policy holder, you can't invest these funds and they don't give retirement revenue for you as they can with entire life insurance policy plans. Nevertheless, the insurer can invest the cash and gain returns.

The following section details the pros and disadvantages of degree term life insurance. Foreseeable costs and life insurance policy coverage Streamlined plan framework Prospective for conversion to irreversible life insurance Minimal protection duration No cash worth accumulation Life insurance policy premiums can boost after the term You'll discover clear advantages when comparing level term life insurance coverage to other insurance policy kinds.

How do I choose the right What Is Level Term Life Insurance??

You constantly understand what to expect with low-priced level term life insurance policy protection. From the minute you secure a plan, your premiums will certainly never transform, assisting you plan financially. Your coverage will not differ either, making these plans efficient for estate planning. If you value predictability of your settlements and the payouts your heirs will obtain, this kind of insurance coverage can be an excellent fit for you.

If you go this route, your costs will raise however it's constantly great to have some adaptability if you wish to maintain an active life insurance coverage policy. Renewable level term life insurance coverage is an additional choice worth considering. These policies enable you to maintain your present strategy after expiration, providing versatility in the future.

{kind=link}

Table of Contents

Latest Posts

Funeral Costs Calculator

Instant Life Insurance Coverage

About Burial Insurance

More

Latest Posts

Funeral Costs Calculator

Instant Life Insurance Coverage

About Burial Insurance